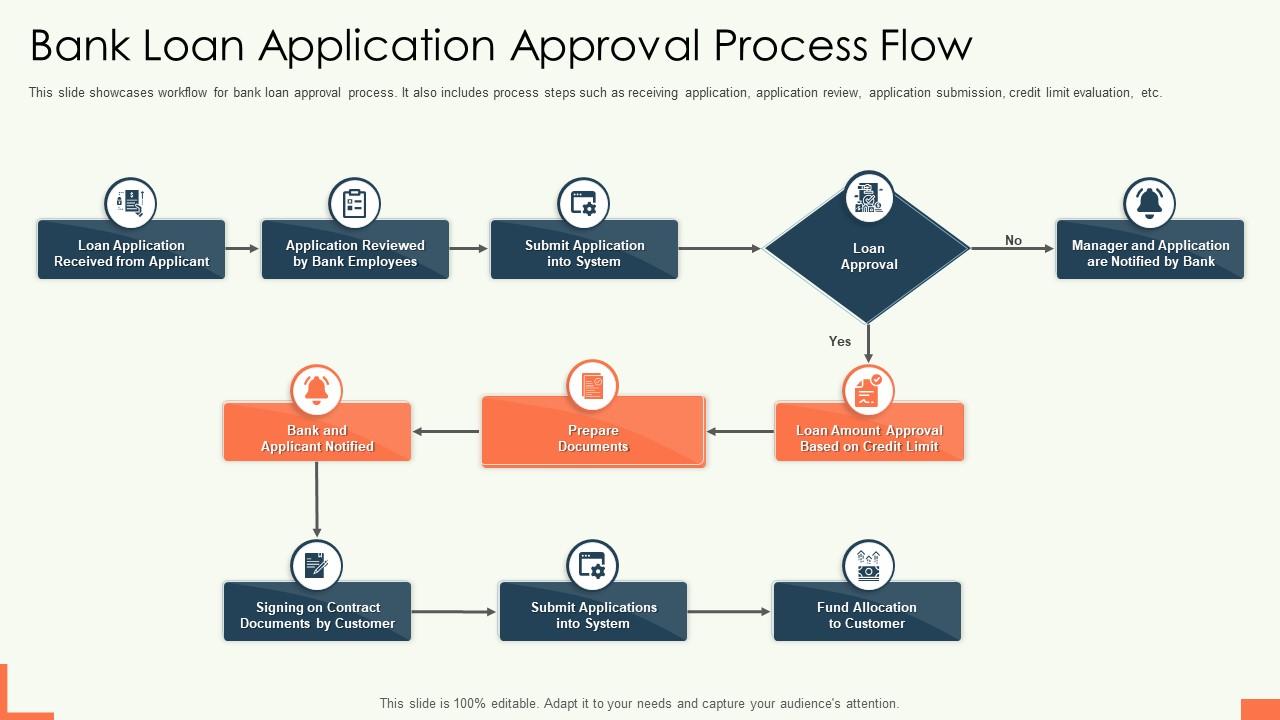

Understanding the Loan Approval Process: A Complete Guide

The loan approval process can often feel overwhelming, especially for those who are unfamiliar with how lenders evaluate applications. However, understanding the steps involved can make the process more transparent and less stressful. Whether you’re applying for a personal loan, business loan, or mortgage, the general framework remains similar. This guide will walk you through each stage of the loan approval process, from application to closing, and provide insights into what you can expect along the way.

Step 1: Gathering and Submitting Application & Required Documents

The first step in any loan application is gathering and submitting the necessary documents. The exact requirements vary depending on the type of loan and the lender’s policies. For example, a personal loan may require proof of income and credit history, while a business loan might need financial statements and tax returns.

Typical documents needed include:

- Personal financial statements

- Authorization to release credit information

- Tax returns or financial statements (for the past 2-3 years)

- Legal entity documents (for business loans)

- Proof of identity and address

Once these documents are collected, they are submitted to the lender, who will then move the application to the next stage.

Step 2: Loan Underwriting

After submission, the loan enters the underwriting phase. During this stage, the lender evaluates the risk associated with the loan. One common method used is the “Five C’s of Credit”: Character, Capital, Capacity, Collateral, and Conditions.

Key factors considered during underwriting include:

- Credit score and history

- Repayment history with other lenders

- Cash reserves and cash flow

- Personal down payment

- Economic and industry conditions

- Collateral offered

The time it takes to complete underwriting depends on the complexity of the loan and the number of parties involved. Some applications may be processed quickly, while others may take longer due to additional documentation or review.

Step 3: Decision & Pre-Closing

Once the underwriting is complete, the lender makes a decision on the loan. If approved, the terms and conditions are communicated to the applicant. These typically include the interest rate, repayment schedule, and any fees associated with the loan.

If the terms are acceptable, the next step is pre-closing, where the lender orders necessary items such as:

- Appraisal

- Survey

- Title insurance

- Loan documents

These items are reviewed to ensure they meet the lender’s requirements before proceeding to the final step.

Step 4: Closing

Closing is the final stage of the loan approval process. At this point, all required documents are signed, and funds are disbursed according to the approval. The closing typically occurs at the lender’s office, a title insurance company, or an attorney’s office.

During closing, applicants receive copies of all signed documents, which serve as a record of the transaction. It’s also an opportunity to ask any remaining questions about the loan terms.

Step 5: Post-Closing

After the loan is closed, the transaction is finalized, and the borrower receives a summary of the loan details. This includes information about the lender, how to access the account, and when payments are due.

Post-closing documents may also include information about membership benefits, if applicable, and how to manage the loan effectively.

Factors That Influence the Loan Approval Process

Several factors can influence the speed and outcome of the loan approval process. These include:

- Credit score: A higher credit score increases the likelihood of approval.

- Income and debt-to-income (DTI) ratio: Lenders assess your ability to repay the loan based on your income and existing debts.

- Collateral: Secured loans may have different requirements compared to unsecured ones.

- Lender policies: Different lenders have varying criteria and processes.

Understanding these factors can help borrowers prepare more effectively and increase their chances of approval.

Tips to Speed Up the Loan Approval Process

To streamline the loan approval process, consider the following tips:

- Prepare documents in advance: Having all necessary paperwork ready can save time.

- Check your credit report: Ensuring accuracy can prevent delays.

- Apply for prequalification: Many lenders offer prequalification to gauge eligibility quickly.

- Provide accurate information: Incomplete or incorrect data can lead to rejections or delays.

By following these steps, borrowers can navigate the loan approval process more efficiently and reduce the risk of complications.

Conclusion

The loan approval process, while complex, is designed to ensure that borrowers are financially capable of repaying the loan. By understanding each step and preparing accordingly, individuals can increase their chances of success. Whether you’re applying for a personal loan, business loan, or mortgage, being informed and proactive is key to a smooth experience.