The Ultimate Guide to Financial Education: Build a Stronger Financial Future

Financial education is the cornerstone of personal and economic stability. It equips individuals with the knowledge and skills needed to make informed decisions about money, from budgeting and saving to investing and planning for retirement. In an increasingly complex financial landscape, understanding how to manage money effectively has never been more critical. This guide explores the importance of financial literacy, strategies for improving it, and the resources available to help you take control of your financial future.

Why Financial Education Matters

Financial literacy is not just about numbers—it’s about empowerment. It enables individuals to navigate the financial world confidently, avoid common pitfalls, and achieve long-term goals. According to the Center for Retirement Research at Boston College, over half of Americans cannot maintain their lifestyle after age 65 due to inadequate retirement savings. This statistic underscores the urgent need for better financial education.

Key Benefits of Financial Literacy

- Improved Decision-Making: Financially literate individuals are better equipped to make informed choices about spending, saving, and investing.

- Debt Management: Understanding how to manage debt responsibly can prevent financial crises and improve credit scores.

- Emergency Preparedness: A solid grasp of financial basics helps build an emergency fund, providing a safety net during unexpected events.

- Retirement Planning: Knowing how to save and invest for the future ensures a more secure retirement.

- Avoiding Fraud: Financial education protects against scams and predatory lending practices.

Strategies to Improve Financial Literacy

Improving financial literacy is a continuous process that requires both learning and practice. Here are some effective strategies to get started:

1. Create a Budget

A budget is the foundation of financial management. Track your income and expenses to understand where your money goes. Use tools like Excel spreadsheets or budgeting apps to stay on top of your finances.

2. Pay Yourself First

Prioritize saving by setting aside a portion of your income before paying other expenses. This habit ensures that you’re consistently building wealth and preparing for the future.

3. Manage Debt Wisely

Develop a plan to pay off high-interest debt, such as credit card balances. Consider consolidating loans or negotiating with creditors to reduce interest rates.

4. Invest for the Future

Start investing early to take advantage of compound interest. Options like 401(k)s and IRAs offer tax advantages and help grow your savings over time.

5. Monitor Your Credit Score

Your credit score impacts your ability to borrow money and access favorable interest rates. Check your credit report regularly and address any errors promptly.

Free Resources for Financial Education

Numerous free resources are available to help individuals enhance their financial knowledge. These include online courses, workshops, and government-sponsored programs.

Online Courses and Workshops

Several platforms offer free financial education courses, including:

– Clever Girl Finance: Offers a “Transform Your Money Mindset” course bundle for beginners.

– Choose FI Foundation: Provides a comprehensive course on achieving financial independence.

– Coursera: Features courses on budgeting, debt management, and investment strategies.

Government and Nonprofit Programs

Organizations like the Consumer Financial Protection Bureau (CFPB) and MyMoney.gov provide free educational materials tailored to different life stages. These resources cover topics such as budgeting, saving, and retirement planning.

The Role of Financial Education in Schools

Financial education should be a standard part of school curricula. While some states require high school students to take personal finance courses, many schools lack the funding and resources to implement comprehensive programs. Advocates like the Jump$tart Coalition argue that financial literacy should be taught before students become adults, ensuring they are prepared to manage their finances independently.

Challenges in School-Based Financial Education

- Funding Constraints: Many school districts struggle to allocate funds for new programs.

- Variability in Curriculum: The quality and availability of financial education vary widely across regions.

- Lack of Trained Educators: Teachers often lack the expertise to teach financial concepts effectively.

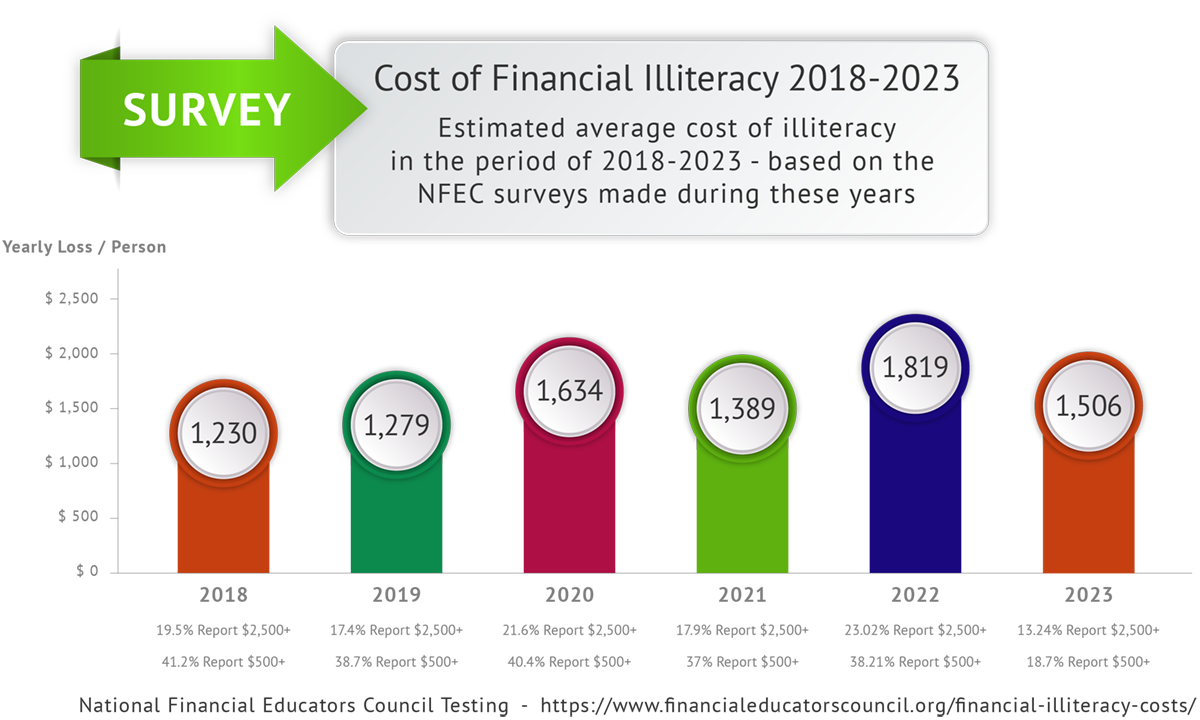

The Impact of Financial Illiteracy

Financial illiteracy can lead to severe consequences, including debt accumulation, poor credit, and financial instability. A 2024 Federal Reserve survey found that 19% of U.S. adults reported being “just getting by” financially, while 8% found it difficult to meet basic needs. These figures highlight the need for widespread financial education.

Common Pitfalls of Financial Illiteracy

- Unmanageable Debt: Poor financial decisions can result in overwhelming debt burdens.

- Inadequate Retirement Savings: Many Americans fail to save enough for retirement, leading to financial insecurity in later years.

- Vulnerability to Scams: Lack of knowledge makes individuals more susceptible to fraud and predatory lending.

Conclusion

Financial education is a vital tool for achieving financial security and independence. By developing financial literacy, individuals can make informed decisions, avoid common pitfalls, and build a stronger financial future. With the right resources and strategies, anyone can improve their financial knowledge and take control of their money. Start today—your future self will thank you.