IMAGE: Best credit card for student needs

The Ultimate Guide to Finding the Best Credit Card for Your Needs

Choosing the best credit card for your needs can be a daunting task. With so many options available, it’s essential to understand what factors matter most and how different cards cater to various lifestyles. Whether you’re a student looking to build credit or an experienced user seeking rewards, this guide will help you navigate the world of credit cards and find the one that fits your financial goals.

What is a Student Credit Card?

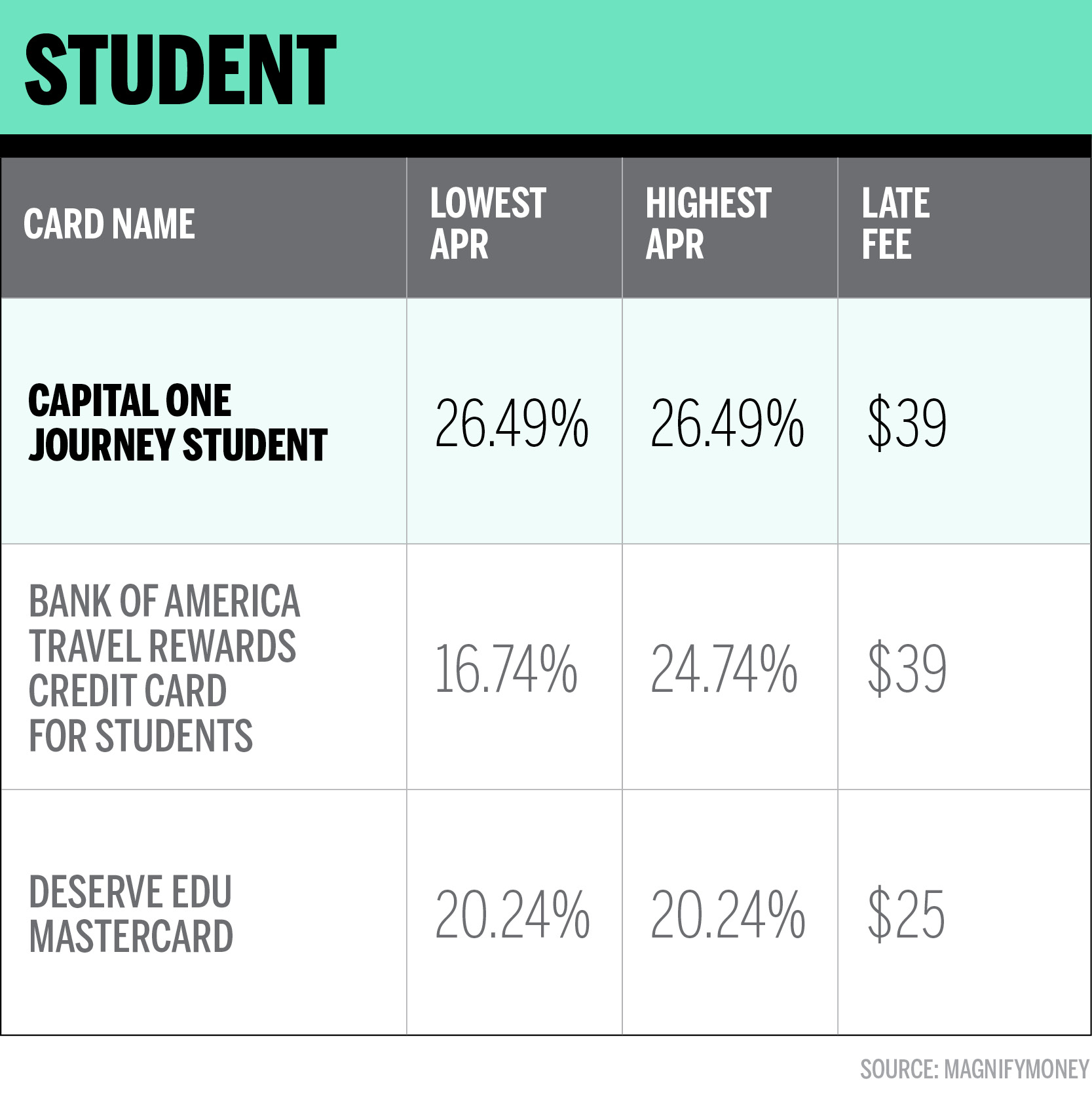

Student credit cards are specifically designed for college students who want to start building their credit history. These cards often have lower credit requirements and offer features tailored to students, such as no penalty APRs, automatic credit limit reviews, and free credit score monitoring. While they may not come with large sign-up bonuses or high credit limits, they are excellent tools for establishing a solid credit foundation.

How to Get Your First Credit Card

Before applying for your first credit card, it’s crucial to check your credit reports and credit score. This will give you a clear picture of your financial standing. Research cards that align with your spending habits and financial goals. Consider factors like annual fees, rewards programs, and APRs. It’s also important to apply for only one card at a time, as multiple applications can negatively impact your credit score.

If you have limited or no credit history, consider alternatives like secured credit cards or becoming an authorized user on a family member’s account. These options can help you build credit while minimizing risk.

Understanding Your Student Credit Card’s Features

When using a student credit card, it’s essential to understand key features like the annual percentage rate (APR), credit limit, and rewards. The APR is the interest rate charged on balances carried from month to month. A higher credit score typically leads to a lower APR. However, the best way to avoid interest is to pay your balance in full each month.

Penalty APRs can come into effect if you fail to make minimum payments. These rates are usually the highest you’ll encounter. Your credit limit is the maximum amount the issuer will extend to you, which is typically $1,000 or less for student cards. Rewards programs vary, but cash back, points, and sign-up bonuses are common.

Pros and Cons of Student Credit Cards

Pros:

– Easy to qualify: Most student cards are accessible to those with varying credit scores, though proof of income may be required.

– Rewards potential: You can earn cash back or other rewards while building credit.

– Student-centric benefits: Many cards offer perks like free FICO score access and student-friendly spending categories.

Cons:

– Pricey APRs: Carrying a balance can be costly due to high interest rates.

– Lack of bonuses: Most student cards don’t offer large sign-up bonuses.

– Ability to overspend: Without proper budgeting, it’s easy to accumulate debt.

Who Should Get a Student Credit Card?

You should consider a student credit card if:

– You regularly shop for books, food, clothes, or other essentials.

– You want to establish your credit history while in school.

– You value student-friendly perks like free credit score access.

Avoid a student credit card if:

– You want to optimize rewards earning.

– You travel frequently.

– You have debt or a tight budget.

How to Make the Most of Your Student Credit Card

Using your student credit card responsibly is key to building good credit. Here are some tips:

– Pay on time: Always meet the due date to avoid late fees and interest charges.

– Keep your balance low: Aim to keep your balance below 30% of your credit limit to maintain a good credit score.

– Track your spending: Use budgeting tools or apps to monitor your purchases and stay within your budget.

– Take advantage of rewards: Use your card for everyday purchases to maximize benefits.

– Monitor your credit score: Many student cards offer free access to your FICO score. Check it regularly to track progress.

– Avoid carrying a balance: Pay off your balance in full each month to avoid interest charges and build credit without debt.

– Use the card responsibly: Treat it as a tool for building credit, not a way to spend beyond your means.

Alternatives to Student Credit Cards

If you’re concerned about qualifying for a student credit card, consider these alternatives:

– Secured credit card: Requires a deposit, which serves as your credit limit. Great for building credit.

– Become an authorized user: Benefit from a family member’s positive credit history without being responsible for the debt.

– Credit builder loan: Helps improve your credit score through timely payments.

– Prepaid debit card: Offers convenience without the risk of debt, though it won’t help build credit.

How We Picked the Best Student Credit Cards

Our editorial team analyzed over 109 student credit cards to identify the top options for young adults and new cardholders. We focused on credit-building perks, affordability, and student-specific benefits. Key criteria included regular APR, foreign transaction fees, sign-up bonuses, credit requirements, rewards rates, and redemption options.

Best Cash Back Credit Cards Compared

Cash back credit cards are a popular choice for those looking to earn rewards on their everyday spending. Here are some of the top options:

Best for 2% Cash Rewards: Wells Fargo Active Cash® Card

- Features: Unlimited 2% flat cash rewards on all purchases. No rotating categories or enrollment required.

- Drawbacks: High APR could lead to hefty interest charges if you carry a balance.

- Alternatives: Chase Freedom Unlimited offers 1.5% cash back on all purchases with additional travel rewards.

Best for Grocery, Gas, and Online Rewards: Blue Cash Everyday® Card from American Express

- Features: Generous cash back in multiple categories, including $7 back monthly on eligible subscriptions.

- Drawbacks: Low cash back on superstores and warehouse clubs.

- Alternatives: Wells Fargo Autograph Card offers six bonus categories with 3X points.

Best for Rotating Categories: Discover it® Cash Back

- Features: Automatically matches cash back earnings at the end of the first year. No foreign transaction fees.

- Drawbacks: Requires tracking of quarterly bonus categories.

- Alternatives: Citi Double Cash offers a flat 2% cash back with no annual fee.

Best for Dining and Entertainment: Capital One Savor Cash Rewards Credit Card

- Features: 3% cash back on dining and grocery purchases. Broad entertainment category coverage.

- Drawbacks: Limited to food and entertainment categories.

- Alternatives: Citi Custom Cash automatically rewards your top spending category.

Best for Flat-Rate Cash Back: Citi Double Cash® Card

- Features: 1% cash back when you purchase and an additional 1% as you pay off. Flexible redemption options.

- Drawbacks: No intro APR offer on purchases.

- Alternatives: Wells Fargo Active Cash offers 2% cash back with an intro APR.

Best for U.S. Supermarkets: Blue Cash Preferred® Card from American Express

- Features: 6% cash back at U.S. supermarkets (up to $6,000 per year). No rotating categories.

- Drawbacks: High spending requirement for the welcome offer.

- Alternatives: Blue Cash Everyday offers similar rewards with no annual fee.

Best for Dining and Drugstores: Chase Freedom Unlimited®

- Features: 1.5% cash back on general spending. Bonus categories for dining and drugstores.

- Drawbacks: Lower cash back rate than other cards.

- Alternatives: Wells Fargo Active Cash offers 2% cash back with no annual fee.

Best for Unlimited Rewards: Capital One Quicksilver Cash Rewards Credit Card

- Features: 1.5% cash back on all purchases. No annual fee.

- Drawbacks: Lower cash back rate compared to other flat-rate cards.

- Alternatives: Chase Freedom Unlimited offers more flexible rewards.

Best for Students: Discover it® Student Cash Back

- Features: Intro APR offer, forgiving rates, and Cashback Match. Ideal for building credit.

- Drawbacks: Rewards program requires more effort.

- Alternatives: Chase Freedom® Student offers a $50 bonus for first-time purchases.

Best for Flat Rate + Sign-Up Bonus: Upgrade Cash Rewards Elite Visa®

- Features: High flat rate on all purchases. Unique sign-up bonus and flexibility.

- Drawbacks: Rewards are automatically applied toward paying off your balance.

- Alternatives: Wells Fargo Active Cash offers a straightforward welcome bonus.

What Are Cash Back Credit Cards?

Cash back credit cards allow you to earn a percentage of your eligible purchases back as cash. Most cards offer between 1% and 5% cash back, depending on the card issuer and spending categories. You can redeem your cash back as a statement credit, direct deposit, gift card, or even charitable donation.

How to Calculate Cash Back

The amount of cash back you earn depends on your card’s terms and your spending. For example, if you spend $1,000 on a card offering 2% cash back, you’d earn $20 in rewards. Some cards have spending limits, so it’s important to review the terms before applying.

Types of Cash Back Cards

There are three main types of cash back cards:

– Flat-rate: Earn a set percentage on all purchases. Simple and straightforward.

– Tiered categories: Higher rewards for specific spending categories. Ideal for frequent shoppers.

– Rotating or customizable bonus categories: Change quarterly or allow you to choose your own. Great for seasonal spending.

How to Compare Cash Back Credit Cards

When choosing a cash back card, consider:

– Cash back rates: Look for cards that offer high rewards on your most common purchases.

– Redemption options: Choose a card that allows flexible redemption, such as statement credits or gift cards.

– Intro APR offers: Some cards offer 0% interest on new purchases for a limited time.

– Fees: Avoid cards with high annual fees or hidden costs.

Cash Back Cards vs. Travel Cards: Which Should You Pick?

Choose a cash back card if:

– You pay your balance in full each month.

– You prefer a straightforward redemption plan.

– You value flexibility in how you use your rewards.

Choose a travel card if:

– You travel frequently.

– You want extra perks like airport lounge access or free checked baggage.

– You’re willing to strategize to maximize your rewards.

How to Choose a Cash Back Credit Card

Consider the following factors:

– Credit score: Most cash back cards require good to excellent credit.

– Cost: Look for cards with low or no annual fees.

– Spending habits: Choose a card that rewards your most common purchases.

– Time commitment: Decide whether you want a simple flat-rate card or one that requires more strategy.

Who Should Get a Cash Back Credit Card

- The strategic spender: Combine flat-rate and tiered cards to maximize rewards.

- The minimalist: A flat-rate card with no annual fee is ideal for simplicity.

- The foodie: Cards like the Capital One Savor or Amex Blue Cash Preferred offer high rewards on dining and groceries.

Who Should Skip a Cash Back Credit Card

- The luxury traveler: Consider a travel card with high-end perks.

- The overspender: Cash back may tempt you to spend more than necessary.

- The credit-builder: Focus on responsible card use rather than rewards.

- The balance carrier: High APRs can quickly deplete your rewards.

Pitfalls to Avoid with a Cash Back Card

- Carrying balances: Pay your balance in full to avoid interest charges.

- Mismatched spending behavior: Choose a card that rewards your top spending categories.

- Missed redemption opportunities: Redeem your rewards regularly to maximize their value.

How to Maximize Your Cash Back Credit Card

- Match yourself with a card that suits your spending habits.

- Strategize spending on bonus categories.

- Pair cards to fill in reward gaps.

- Pay your balances in full each month.

- Utilize a sign-up bonus.

- Check the card’s online shopping portals.

- Make the most of an intro APR offer.

Alternatives to Cash Back Credit Cards

If cash back isn’t the right fit for you, consider:

– Travel cards: Offer rewards for travel-related purchases.

– Student cards: Ideal for building credit with no annual fees.

– Low-interest cards: Save money by avoiding high interest charges.

– Starter/credit builder cards: Help improve your credit score from scratch.

How We Picked the Best Cash Back Credit Cards

We evaluated cards based on:

– Cash back rate and categories: High rewards on common purchases.

– Redemption options: Flexible ways to use your rewards.

– Sign-up bonus: Generous rewards for low spending thresholds.

– Rates and fees: Avoid cards with sky-high interest rates.

– Miscellaneous benefits: Additional perks like price protection or auto rental insurance.

Conclusion

Finding the best credit card for your needs requires careful consideration of your financial goals, spending habits, and lifestyle. Whether you’re a student building credit or a seasoned user looking for rewards, there’s a card out there that fits your unique situation. By understanding the features, pros, and cons of different cards, you can make an informed decision that helps you achieve your financial objectives.