The Ultimate Guide to Effective Financial Management for Personal and Business Success

Financial management is a critical skill that empowers individuals and businesses to achieve stability, growth, and long-term success. Whether you’re managing personal finances or steering a company’s financial strategy, understanding how to effectively manage money is essential. This guide will walk you through the key steps of financial management, from budgeting and saving to investing and planning for the future.

Understanding Your Current Finances

The first step in effective financial management is gaining a clear understanding of your current financial situation. Start by listing all your income sources, including salaries, side gigs, and investments. Then, track your monthly expenses across different categories such as housing, utilities, groceries, transportation, and entertainment.

This process helps you identify where your money is going and whether you’re spending more than you earn. It also allows you to spot areas where you can cut back or reallocate funds. Additionally, reviewing your credit report and score can reveal hidden debts or errors that may impact your financial health.

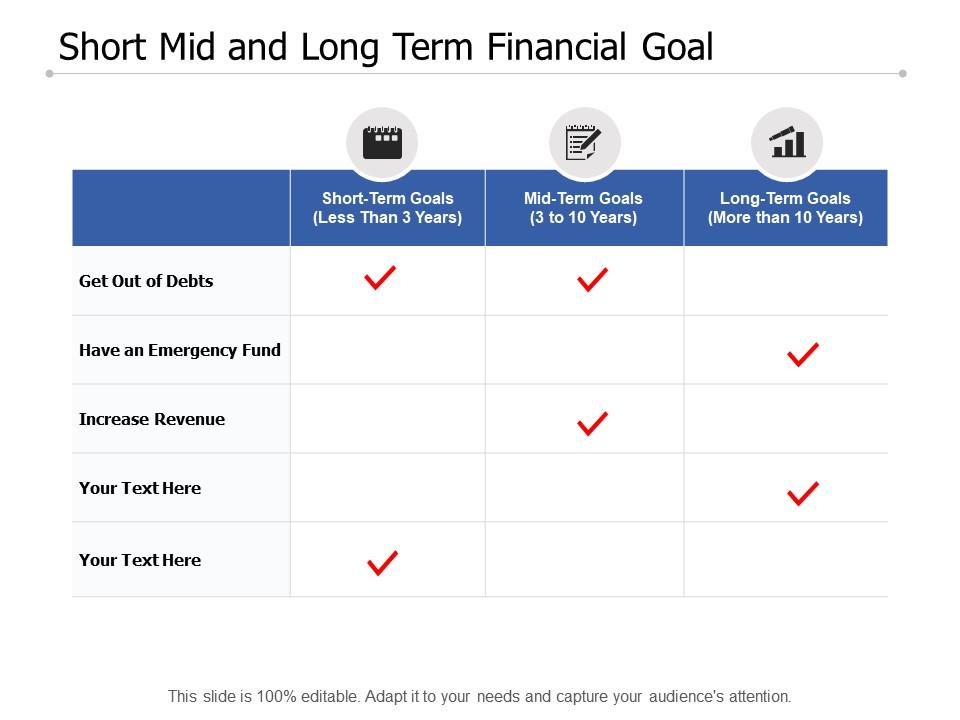

Defining Your Financial Goals

Once you have a clear picture of your finances, the next step is to define your financial goals. These can be short-term, medium-term, or long-term, depending on your needs and aspirations. Short-term goals might include paying off credit card debt or saving for a vacation, while long-term goals could involve buying a home, starting a business, or retiring comfortably.

It’s important to set specific, measurable, and achievable goals. For example, instead of saying “I want to save money,” aim for something like “I want to save $5,000 for a down payment on a car in 12 months.” Prioritizing your goals based on urgency and importance ensures that you focus on what matters most.

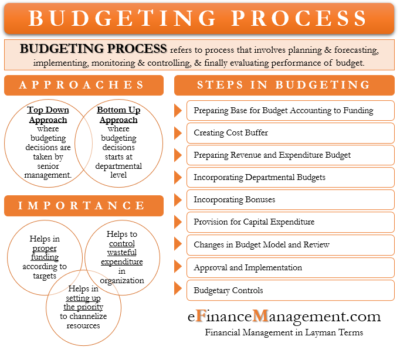

Creating a Realistic Budget

A well-structured budget is the foundation of effective financial management. Start by allocating funds for essential expenses such as rent, utilities, and groceries. Then, plan for debt repayment and savings contributions. Finally, assign money for discretionary spending.

There are various budgeting methods to choose from, such as the 50/30/20 rule, which divides your income into 50% for essentials, 30% for discretionary spending, and 20% for savings and debt repayment. Alternatively, zero-based budgeting assigns every dollar a purpose, giving you total control over your spending. Experiment with different methods to find one that works best for you.

Building an Emergency Fund

Life is unpredictable, and unexpected expenses can disrupt even the best-laid financial plans. An emergency fund serves as a safety net for events such as medical bills, car repairs, or temporary unemployment. Aim to save three to six months of living expenses in an accessible account. If this target seems daunting, start with a smaller goal and build gradually.

Place your emergency fund in a separate account to avoid the temptation to spend it on non-emergencies. High-yield savings accounts can offer interest while keeping the money liquid. If you do need to use your emergency fund, replenish it as soon as possible to maintain financial security.

Saving and Investing for the Future

After establishing an emergency fund, focus on long-term savings and investments. Retirement accounts such as 401(k)s or IRAs offer tax advantages and allow for compound growth over time. Take full advantage of employer matching contributions whenever they’re available.

Beyond retirement, consider investing in college funds, real estate, or entrepreneurial ventures. Diversifying your investments reduces the impact of market fluctuations and provides potential growth over decades. Consult with a financial advisor to create a personalized investment strategy that aligns with your risk tolerance and financial goals.

Reviewing and Improving Your Plan

Financial management is an ongoing process that requires regular review and adjustment. Schedule a review of your finances once a year to evaluate your spending, debt, savings, and investments. Use tools like financial apps or spreadsheets to simplify this process and make informed decisions.

Stay flexible and open to change. Life circumstances, income levels, and goals can evolve over time, so regularly updating your financial plan ensures that it continues to reflect your current situation. Minor adjustments and consistent monitoring can yield substantial improvements in your financial stability and confidence.

Conclusion

Effective financial management is a powerful tool that can help you achieve personal and business success. By understanding your current finances, defining clear goals, creating a realistic budget, building an emergency fund, saving and investing for the future, and regularly reviewing your plan, you can take control of your financial destiny. With discipline, consistency, and informed decision-making, you’ll be well on your way to achieving long-term financial stability and growth.