Understanding Inheritance Tax: What You Need to Know

Inheritance tax is a complex and often misunderstood aspect of estate planning. It refers to the tax imposed on the transfer of property or assets from a deceased individual to their heirs. While it may seem like a straightforward concept, the intricacies of how it’s calculated, who is responsible for paying it, and which states impose it can be confusing. This article aims to provide a comprehensive overview of inheritance tax, its implications, and what you need to know if you’re an heir or considering estate planning.

The Basics of Inheritance Tax

At its core, an inheritance tax is a levy placed on the recipient of inherited assets. Unlike an estate tax, which is paid by the estate itself, the inheritance tax is directly owed by the beneficiary. This distinction is crucial because it affects who is legally responsible for the payment and how the tax is calculated.

The tax is typically based on the value of the assets received and the relationship between the heir and the deceased. Close relatives, such as spouses and children, often face lower tax rates or even exemptions, while distant relatives or non-relatives may be subject to higher rates. This kinship-based approach sets inheritance tax apart from other forms of taxation, which are generally based on income or property value rather than familial ties.

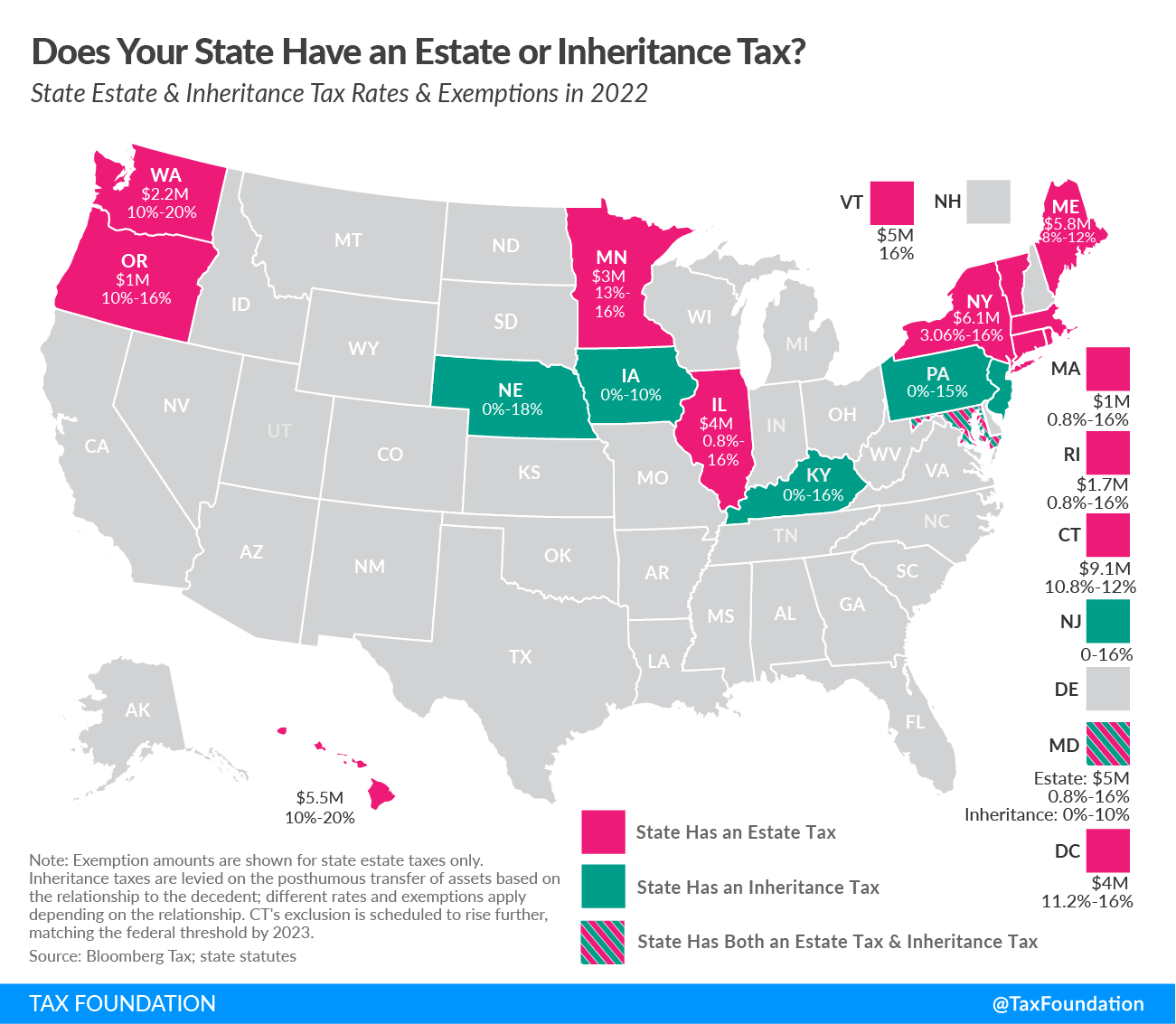

Which States Impose Inheritance Tax?

It’s important to note that not all U.S. states impose an inheritance tax. In fact, only a handful of states currently have this type of tax in place. As of now, the following states levy an inheritance tax:

- Kentucky

- Maryland

- Nebraska

- New Jersey

- Pennsylvania

Iowa previously had an inheritance tax, but it was phased out and fully repealed as of 2025. Maryland stands out as the only state that imposes both an inheritance tax and a state-level estate tax, making it unique in its approach to post-mortem taxation.

Key Differences Between Inheritance Tax and Estate Tax

One of the most common sources of confusion is the difference between inheritance tax and estate tax. While both are taxes related to the transfer of wealth after someone’s death, they serve different purposes and are applied differently.

-

Estate Tax: This tax is levied on the total value of the deceased person’s estate before it is distributed to heirs. The estate itself is responsible for paying the tax, usually through the executor or personal representative.

-

Inheritance Tax: This tax is imposed on the recipient of the assets. The heir is responsible for paying the tax, and the rate depends on their relationship to the deceased.

Understanding this distinction is essential for proper estate planning. For example, if a person’s estate is subject to the federal estate tax, it may still be exempt from an inheritance tax depending on the state where the deceased lived or owned property.

How Inheritance Tax Is Calculated

The calculation of inheritance tax varies by state, but most use a tiered system based on the beneficiary’s relationship to the decedent. Here’s a general breakdown of how it works:

- Close Relatives (Spouses, Children, Grandchildren): Often receive significant exemptions or lower tax rates.

- Distant Relatives (Siblings, Nieces, Nephews): May face moderate tax rates.

- Non-Relatives (Friends, Charities, Strangers): Typically face the highest tax rates.

For example, in Pennsylvania, transfers to a surviving spouse are taxed at 0%, while transfers to siblings are taxed at 12%. In New Jersey, the top marginal tax rate can reach 16% for certain non-exempt beneficiaries.

Filing and Paying the Tax

Once the tax liability is determined, the executor or administrator of the estate must file the appropriate tax return with the state. Deadlines vary by state, but they are typically within several months of the decedent’s death. For instance, in Pennsylvania, the Inheritance Tax Return (Form REV-1500) must be filed within nine months of the date of death.

Failure to meet the deadline can result in penalties and interest charges. In New Jersey, for example, unpaid taxes accrue interest at an annual rate of 10%. Some states offer small discounts if the tax is paid within a specific timeframe, such as a 5% discount for payments made within three months of the decedent’s death.

Planning Ahead: Strategies to Minimize Tax Liability

Given the potential financial impact of inheritance tax, it’s wise to consider strategies to minimize your tax liability. Here are some common approaches:

- Gifting During Lifetime: Transferring assets while you’re still alive can reduce the taxable estate.

- Establishing Trusts: Certain types of trusts can help protect assets from inheritance tax.

- Charitable Donations: Leaving assets to registered charities can eliminate or reduce tax liability.

- Life Insurance Policies: These can provide liquidity to pay off any inheritance tax obligations.

Conclusion

Inheritance tax is a critical component of estate planning that many individuals overlook. Understanding how it works, which states impose it, and how it differs from other taxes can help you make informed decisions about your financial future. Whether you’re an heir or planning your own estate, being aware of these details can save you time, money, and potential legal complications down the line.

By staying informed and working with a qualified estate planner, you can navigate the complexities of inheritance tax with confidence and ensure that your legacy is protected.