Essential Steps to Manage Personal Finances for Beginners in the United Kingdom

Managing personal finances is a critical skill that ensures stability and long-term security. In the United Kingdom, where financial responsibilities can be complex, understanding how to manage your money effectively is more important than ever. Whether you’re just starting out or looking to improve your current financial habits, there are several key steps you can take to build a solid foundation.

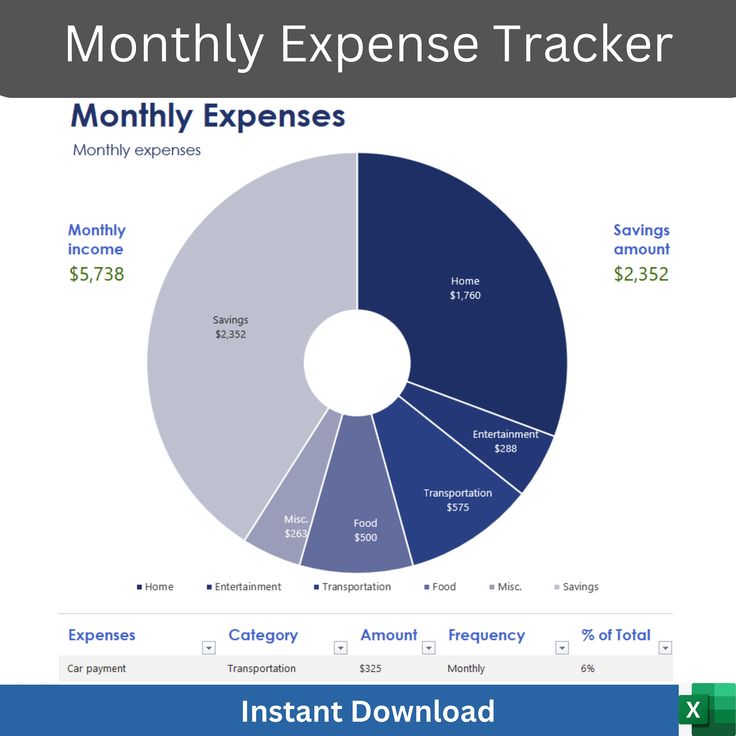

Creating a Budget: The First Step to Financial Control

The first step in managing your finances is creating a budget. A well-structured budget helps you track your income and expenses, ensuring you don’t overspend. Start by listing all your sources of income, such as your salary, side hustles, or any other regular payments. Then, categorize your monthly expenses into essentials like rent, utilities, groceries, and transportation, as well as discretionary spending on entertainment or dining out.

It’s essential to differentiate between needs and wants. For example, while groceries are a necessity, eating out multiple times a week is a want. Setting clear spending limits for each category will help you stay within your means. By consistently reviewing and adjusting your budget, you’ll gain better control over your financial situation.

Starting to Save: Building a Financial Safety Net

Saving is another crucial aspect of personal finance management. While it may seem simple, saving regularly can make a significant difference in your financial health. Begin by setting aside a portion of your income each month, even if it’s just a small amount. Over time, these savings can accumulate and serve as an emergency fund.

To make saving easier, consider cutting down on unnecessary expenses and reallocating that money toward your savings. Consistency is key—by making saving a habit, you’ll be better prepared for unexpected costs, such as car repairs or medical bills. Additionally, having a financial cushion can provide peace of mind and reduce stress during uncertain times.

Managing Debt Wisely: Understanding the Difference Between Good and Bad Debt

Debt is a common part of life, but it’s important to manage it wisely. Not all debt is bad; some types, like mortgages or student loans, can be beneficial in the long run. However, high-interest credit card debt or loans for non-essential purchases can quickly become a burden.

When considering debt, it’s important to distinguish between productive and consumptive debt. Productive debt, such as a business loan or mortgage, can generate assets or increase your earning potential. On the other hand, consumptive debt, like using a credit card for luxury items, only provides temporary satisfaction without long-term benefits. Always ensure that any debt you take on is within your means and aligns with your financial goals.

Investing for the Future: Growing Your Wealth

Investing is a powerful way to grow your wealth over time. By allocating a portion of your income into investments such as stocks, bonds, or mutual funds, you can potentially earn returns that outpace inflation. However, it’s important to understand the risks involved and choose investments that match your risk tolerance.

For beginners, starting with low-risk options like index funds or exchange-traded funds (ETFs) can be a good approach. As you gain more confidence, you can explore other investment opportunities. Remember, investing isn’t just about numbers—it’s also about discipline and patience. Avoid making impulsive decisions based on market fluctuations and focus on long-term growth.

Improving Financial Literacy: Educating Yourself for Better Decisions

Financial literacy plays a vital role in managing your money effectively. Understanding concepts like compound interest, diversification, and risk management can help you make informed decisions. You can start by reading books or articles on personal finance, attending workshops, or taking online courses.

Additionally, consulting a financial advisor can provide personalized guidance tailored to your unique circumstances. Whether you’re planning for retirement, buying a home, or building an emergency fund, having a solid understanding of finance will empower you to make smarter choices.

Exploring Additional Income Sources: Increasing Your Earnings

In addition to managing your existing income, exploring additional revenue streams can accelerate your financial goals. Consider side gigs such as freelancing, selling products online, or offering services in your area of expertise. These opportunities can provide extra income without requiring a full-time commitment.

If you have the capital and time, starting a small business or investing in real estate could also be viable options. However, it’s important to conduct thorough research and assess the risks before diving into any new venture.

Staying Disciplined: The Key to Long-Term Success

Finally, maintaining discipline and consistency is essential for long-term financial success. Set clear goals, such as saving for a house, funding your retirement, or paying off debt. Regularly review your progress and adjust your strategies as needed.

By staying committed to your financial plan, you’ll be better equipped to handle unexpected challenges and achieve your objectives. Remember, small, consistent actions can lead to significant results over time.

In conclusion, managing personal finances requires a combination of planning, discipline, and education. By following these steps, you can build a secure financial future and enjoy greater freedom and peace of mind. Whether you’re just starting out or looking to refine your approach, the principles outlined here can guide you toward financial stability in the United Kingdom.