Understanding the 401(k) Plan: A Comprehensive Guide for UK Residents

A 401(k) plan is a tax-advantaged retirement savings vehicle that has become a cornerstone of financial planning in the United States. While primarily an American concept, its principles and benefits can offer valuable insights for UK residents seeking to build a secure financial future. This article explores what a 401(k) plan is, how it works, and the key considerations for those looking to incorporate similar strategies into their retirement planning.

What Is a 401(k) Plan?

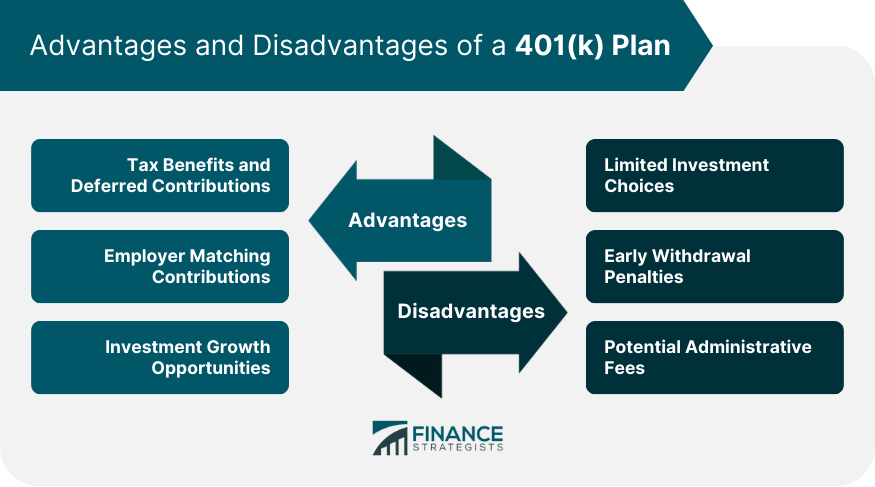

A 401(k) plan is a defined-contribution retirement account established by an employer. Named after a section of the U.S. Internal Revenue Code, these plans allow employees to contribute a portion of their salary directly into an investment account. Employers may also match a percentage of these contributions, effectively boosting the employee’s retirement savings. The primary advantage of a 401(k) is its tax benefits, which can significantly enhance long-term wealth accumulation.

There are two main types of 401(k) plans: traditional and Roth. Traditional 401(k)s allow pre-tax contributions, reducing taxable income in the year they are made. However, withdrawals during retirement are taxed as ordinary income. In contrast, Roth 401(k)s require after-tax contributions, meaning there is no immediate tax deduction. But qualified withdrawals in retirement are tax-free, making them an attractive option for those expecting higher tax rates in the future.

How Do 401(k) Plans Work?

Traditional 401(k) plans were introduced in the early 1980s, allowing employees to make pretax contributions from their salaries up to certain limits. When an employee signs up for a 401(k), they agree to deposit a percentage of each paycheck directly into an investment account. Employers often match part or all of that contribution, providing a powerful incentive to save.

Employees choose the specific investments held within their 401(k) accounts from a selection offered by their employer. These typically include stock and bond mutual funds, target-date funds, and other options designed to align with the employee’s risk tolerance and retirement timeline.

For self-employed individuals or small business owners, a solo 401(k) plan offers a similar structure, allowing them to fund their own retirement without the need for an employer. These plans are particularly beneficial for those who want to maximize contributions while maintaining control over their investment choices.

Key Features and Benefits

One of the most significant advantages of a 401(k) plan is the potential for employer matching contributions. Many employers offer a match, which can be a substantial boost to retirement savings. For example, an employer might match $0.50 for every $1 contributed, up to a certain percentage of the employee’s salary. This is essentially free money, and failing to take advantage of it can leave a significant amount of wealth on the table.

Another benefit is the tax-deferred growth of investments. With a traditional 401(k), earnings grow tax-free until withdrawal, while Roth 401(k)s offer tax-free withdrawals in retirement. This feature can lead to substantial long-term gains, especially when combined with compounding interest.

Contribution Limits and Rules

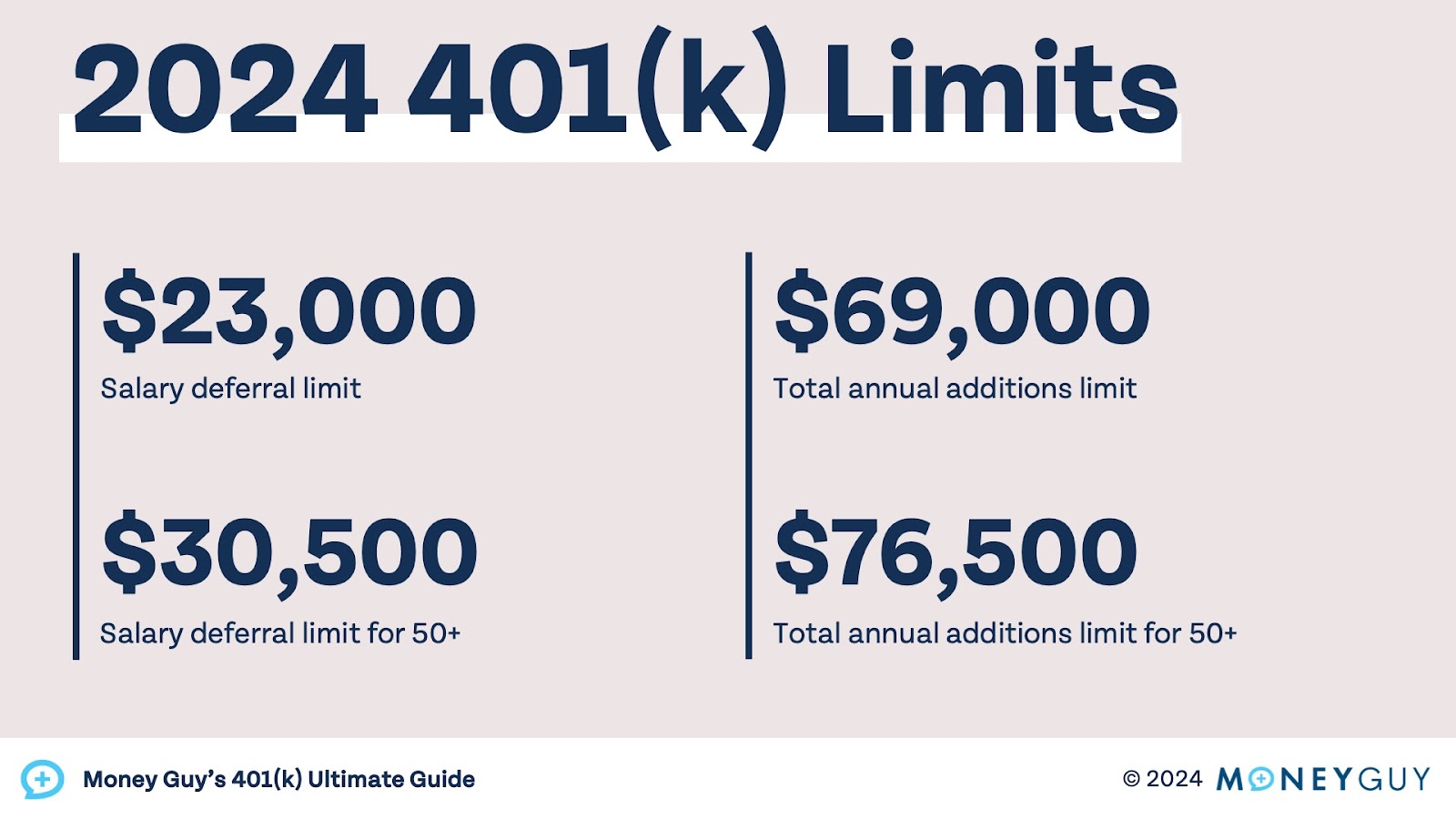

The IRS sets annual limits on contributions to 401(k) plans. For 2025, the maximum contribution for employees under 50 is $23,500, with an additional $7,500 catch-up contribution allowed for those aged 50 and older. Combined employer and employee contributions are capped at $70,000 for those under 50 and $77,500 for those 50 and older.

It is important to note that early withdrawals from a 401(k) before age 59½ are subject to a 10% penalty, along with income taxes. Exceptions exist for certain hardship situations, such as medical expenses or first-time home purchases, but these should be considered carefully due to the long-term impact on retirement savings.

What Happens When You Leave a Job?

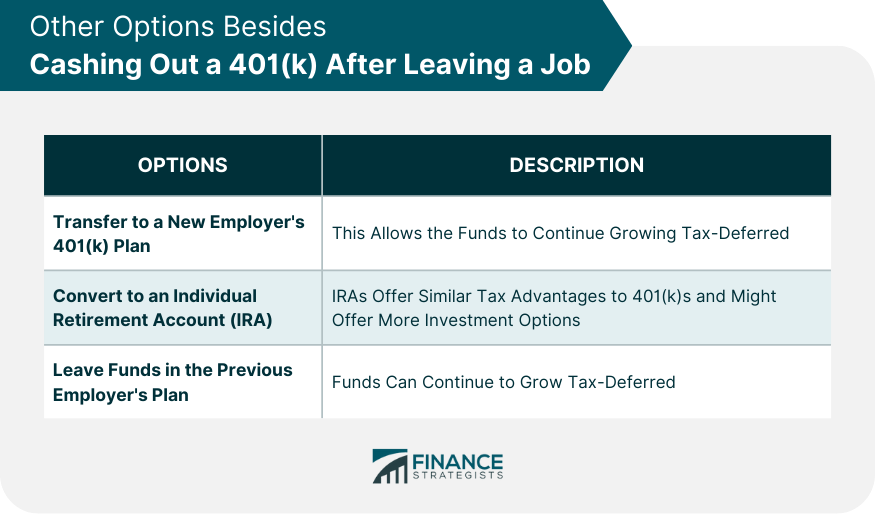

When an employee leaves a job, they have several options for their 401(k) account:

- Withdraw the Money: This is generally not advisable unless absolutely necessary, as it incurs taxes and penalties.

- Roll Over to an IRA: This allows continued tax-deferred growth and access to a wider range of investment options.

- Leave It with the Former Employer: If the account balance is large enough, some employers allow employees to keep their 401(k) indefinitely.

- Move to a New Employer’s Plan: This maintains the tax-deferred status and avoids immediate taxes.

Comparing 401(k) Plans to Other Investment Vehicles

While 401(k) plans are designed specifically for retirement savings, they differ from other investment vehicles like brokerage accounts. Brokerage accounts offer more flexibility in terms of investment choices and no contribution limits, but they lack the tax advantages of a 401(k). Additionally, 401(k)s often come with employer matches, which are not available in standard brokerage accounts.

Conclusion

A 401(k) plan is a powerful tool for building long-term retirement savings, offering tax advantages, employer contributions, and the potential for significant growth. While primarily an American concept, the principles behind 401(k) plans can provide valuable lessons for UK residents looking to secure their financial future. By understanding how these plans work and leveraging their benefits, individuals can create a robust retirement strategy that aligns with their financial goals.