What Is a 401(k)? A Complete Guide to Understanding Retirement Savings

A 401(k) plan is one of the most popular retirement savings vehicles in the United States, offering employees a structured way to save for their future. Named after the Internal Revenue Code section that governs it, a 401(k) allows individuals to contribute a portion of their paycheck to a tax-advantaged retirement account. These plans are typically offered by employers, and many provide matching contributions, making them a powerful tool for long-term financial planning.

Whether you’re just starting your career or nearing retirement, understanding how a 401(k) works can help you make informed decisions about your financial future. This guide will walk you through the basics, including how it functions, the different types available, contribution limits, and more.

How Does a 401(k) Work?

At its core, a 401(k) is an employer-sponsored retirement account that lets employees set aside money from each paycheck. The funds are then invested in a range of options, such as mutual funds, stocks, or bonds, depending on what the employer’s plan offers. Here’s a breakdown of the process:

1. Enrollment and Contributions

When you enroll in a 401(k), you decide how much of your paycheck to contribute. This amount is automatically deducted before taxes (for traditional 401(k)s) or after taxes (for Roth 401(k)s). You can also choose to adjust your contribution rate at any time, subject to plan rules.

2. Investment Options

Once your money is in the account, it grows through investments. The goal is to build wealth over time, with the potential for compounding returns. Most 401(k) plans offer a variety of investment choices, including target-date funds, index funds, and other mutual funds.

3. Tax Advantages

Traditional 401(k)s allow pre-tax contributions, which reduce your taxable income for the year. Roth 401(k)s, on the other hand, use after-tax dollars, but qualified withdrawals in retirement are tax-free. Both options offer tax-deferred growth, meaning you don’t pay taxes on investment gains while the money remains in the account.

4. Employer Match

Many employers offer a matching contribution, which is essentially free money added to your account. For example, if your employer matches 50% of your contributions up to 6% of your salary, contributing 6% would result in a 3% match from your employer.

Types of 401(k) Plans

There are two main types of 401(k) plans: traditional and Roth. Each has its own benefits and drawbacks, depending on your financial situation and retirement goals.

Traditional 401(k)

- Contributions: Made with pre-tax dollars.

- Tax Treatment: Reduces current taxable income.

- Withdrawals: Taxed as ordinary income in retirement.

- RMDs: Required minimum distributions (RMDs) must be taken after age 73.

Roth 401(k)

- Contributions: Made with after-tax dollars.

- Tax Treatment: No immediate tax deduction, but qualified withdrawals are tax-free.

- Withdrawals: Tax-free in retirement, provided you meet certain conditions.

- RMDs: No required minimum distributions.

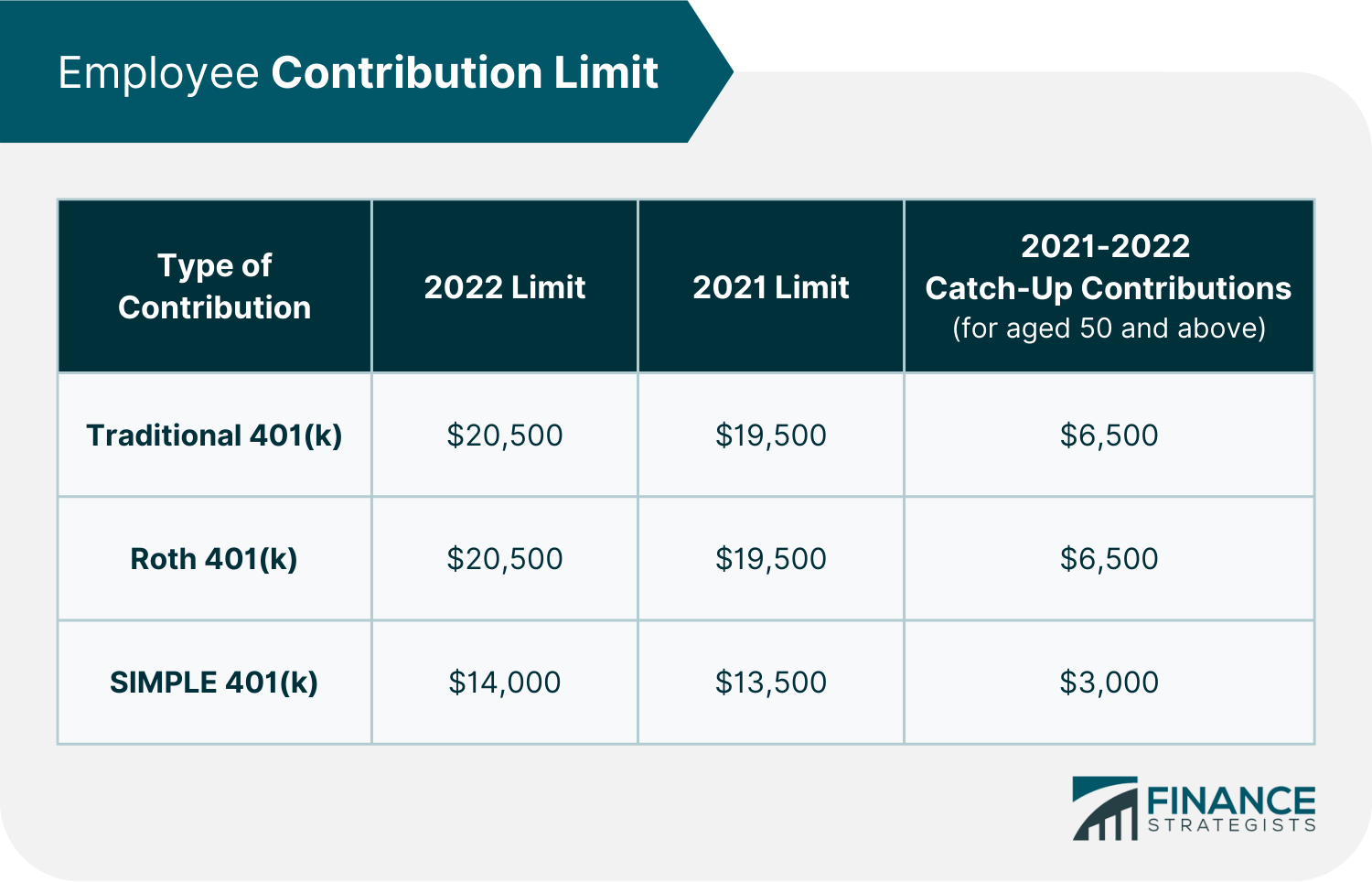

Contribution Limits

The IRS sets annual limits on how much you can contribute to a 401(k). For 2025, the limit is $23,500 for individuals under 50 and $31,000 for those 50 and older (including catch-up contributions). Employers may also contribute, but the total combined limit is $70,000 for those under 50 and $77,500 for those 50 and older.

These limits are higher than those for IRAs, making 401(k)s a more flexible option for high earners. However, it’s important to note that contributions are not tax-deductible for Roth 401(k)s.

Pros and Cons of a 401(k)

Pros

- Tax advantages: Traditional 401(k)s reduce taxable income, while Roth 401(k)s offer tax-free withdrawals in retirement.

- Employer match: Many employers offer matching contributions, which can significantly boost your savings.

- Higher contribution limits: Compared to IRAs, 401(k)s allow for larger annual contributions.

Cons

- Early withdrawal penalties: Taking money out before age 59½ may result in taxes and a 10% penalty.

- Limited investment choices: Your options depend on what your employer offers.

- RMD requirements: Traditional 401(k)s require you to take distributions once you reach a certain age.

Withdrawal Rules

Understanding when and how you can access your 401(k) is crucial. Here are some key points:

- Age 59½: You can withdraw funds without penalty.

- Hardship withdrawals: Some plans allow early withdrawals for specific emergencies, but these may still incur taxes.

- Required Minimum Distributions (RMDs): Traditional 401(k) holders must begin taking RMDs at age 73.

If you leave your job, you have several options: roll the funds into a new 401(k), transfer them to an IRA, or leave them in the old plan (though you won’t be able to contribute further).

401(k) Loans

Some 401(k) plans allow participants to take loans from their accounts. Typically, you can borrow up to 50% of your vested balance or $50,000, whichever is less. The loan must be repaid within five years, and interest is paid back into the account.

While this can be a useful option for short-term needs, it carries risks. If you leave your job, the loan may need to be repaid immediately, and defaulting on the loan could result in taxes and penalties.

Frequently Asked Questions

Can I Lose Money in a 401(k)?

Yes, because the money is invested, there is always a risk of loss based on market fluctuations. However, diversifying your investments can help mitigate this risk.

What Happens to My 401(k) If I Quit My Job?

You can roll the funds into a new 401(k) or an IRA, or leave them in the old plan. However, you won’t be able to contribute further to the old plan.

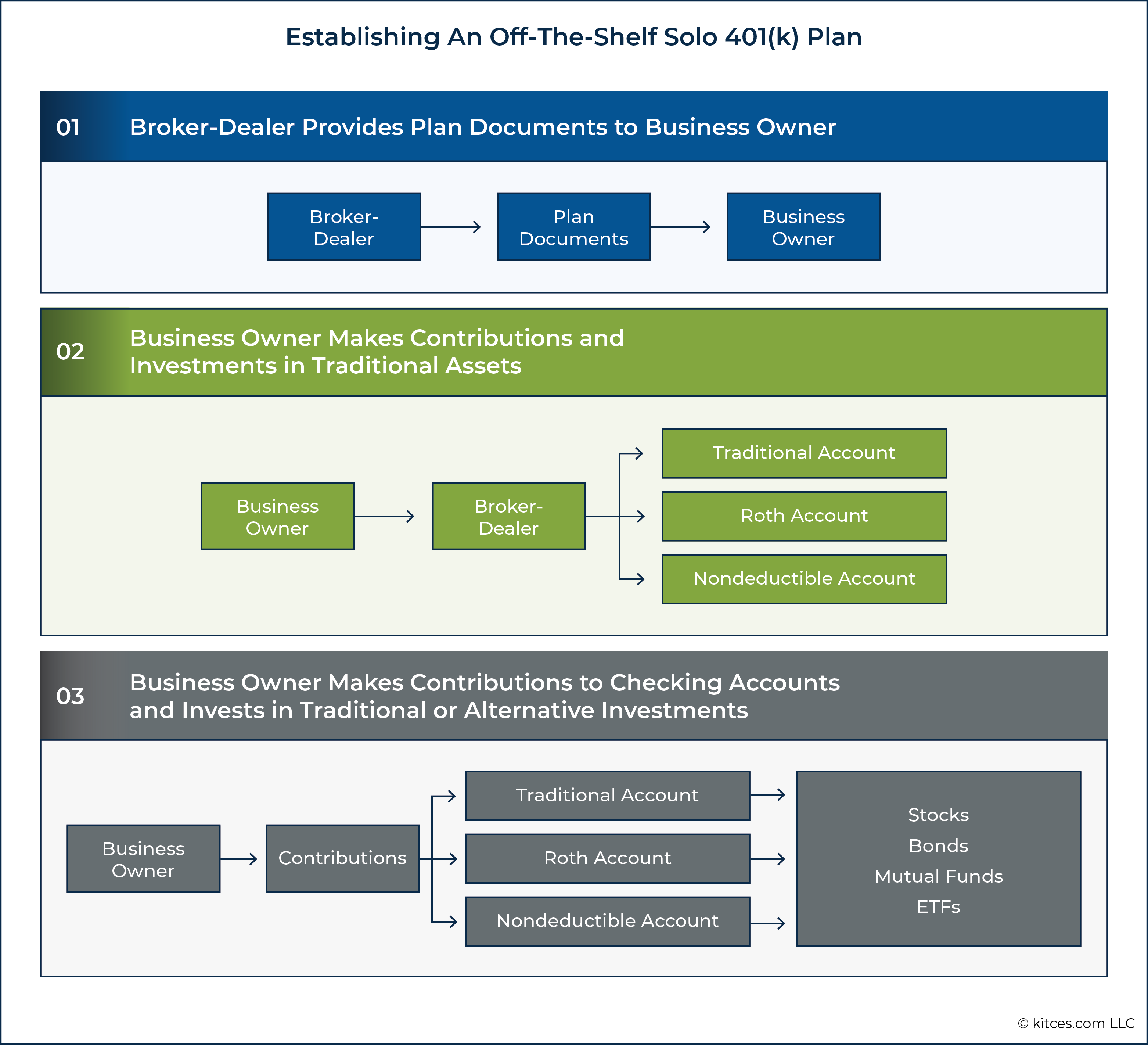

What Is a Solo 401(k)?

A solo 401(k) is a retirement plan designed for self-employed individuals or small business owners with no employees. It allows both employee and employer contributions, offering flexibility for those who don’t have access to a traditional 401(k).

Conclusion

A 401(k) is a powerful tool for building a secure financial future. Whether you’re looking to maximize employer matches, take advantage of tax benefits, or simply start saving for retirement, understanding the ins and outs of a 401(k) can make all the difference. By choosing the right plan, contributing consistently, and making informed investment decisions, you can set yourself up for a comfortable retirement.